Mark Carney is burying the country under a mountain of debt. The latest federal government budget, tabled on Nov. 4, 2025, is slated to pile on an astonishing $320 billion in new debt in the next five years.

All this spending—the bulk of which will be spent on handouts to big business and “defence”—is supposed to “supercharge growth” and stabilize Canada’s swiftly collapsing economy. If this growth does not materialize, this debt mountain threatens a catastrophe for the working class, one that would put explosive class struggle on the agenda.

A mountain of debt

Carney’s deficit spending puts the deficit for 2025–26 alone at $78.3 billion, the largest in history for any non-pandemic year. By 2030 a total of $320 billion in new debt will be added to the national balance sheet. This is on top of an already astronomical gross debt-to-GDP ratio of 111 per cent.

This is a tremendous increase to the already massive mountain of debt accumulated since the 2008 financial crisis. For years, bourgeois economists argued that the debt was not a problem because interest rates were at rock bottom. They imagined this state of affairs could be maintained forever. But now the days of near-zero interest rates are gone, and even the most near-sighted economist knows they aren’t coming back.

Interest payments on the existing debt are swallowing a huge part of the government’s budget. In 2016, debt servicing cost $21.8 billion; this year, it will reach $55.6 billion; by 2029, $76.1 billion—more than the cost of federal transfer payments for health care and child care combined.

Debt-death spiral

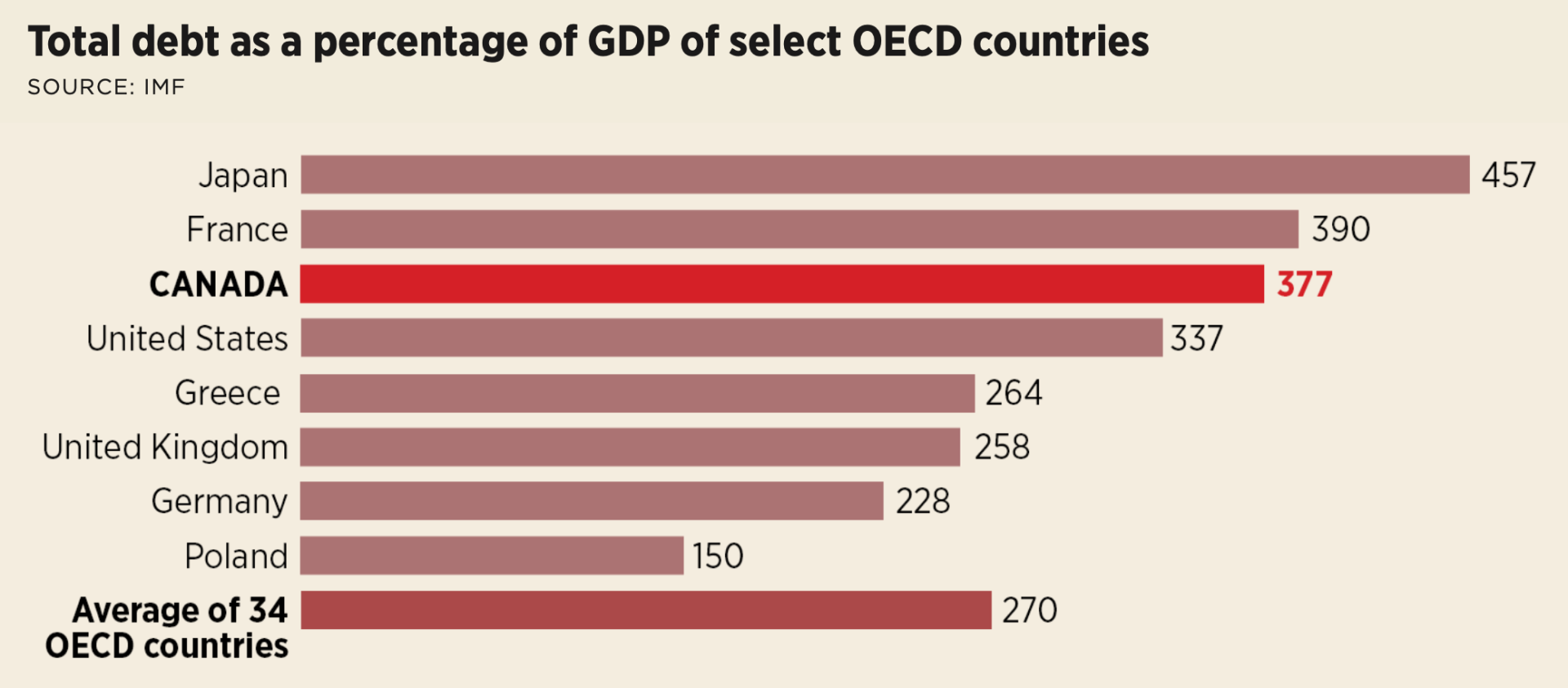

But the worst is yet to come. With the combined federal and provincial debt already at 111 per cent of GDP, Canada is entering the danger zone.

Canada’s debt situation is rapidly becoming comparable to that of France, where the debt stands at 117 per cent, and the government spends nearly 10 per cent of its budget on interest payments. There, the government has tried to solve the crisis by brutal means: lengthening the working day, raising the retirement age, and making vicious cuts to social services.

This has sparked one of the largest political crises—and mass movements—in the history of modern France. And yet the government is hell-bent on carrying it out. The reason for this is simple: only a madman would lend money to someone he thinks is unlikely to pay it back. The French ruling class is desperate to maintain its reputation with investors.

If it fails to do so, the result is what hedge-fund billionaire Ray Dalio calls a “debt-death spiral”. As debt rises and interest payments consume an ever-growing proportion of the budget, sooner or later bond market investors—those who lend the government money—will lose confidence in the government’s ability to pay their debts. Lenders who think the government is at risk of missing payments demand higher interest rates. Interest payments consume more of the budget, and more borrowing is required. With the budget in an even worse state, lenders demand even higher interest rates. Borrowing costs spiral into the stratosphere. Unless drastic action is taken, the government cannot pay the interest and thus defaults on its loans.

Many countries have suffered this fate. Now Dalio is warning that some of the richest countries in the world, like the U.S. and Britain, could be treading the same path and that a debt-death spiral is inevitable for any country that doesn’t bring its deficit spending under control.

The 1995 Canadian debt crisis

Will Canada experience a debt-death spiral? It is possible. To avert it, the government has to get the money from somewhere. If they try to tax the capitalists, the capitalists will invest abroad, weakening the economy. This paradoxically lowers tax revenue, making the debt crisis worse. Therefore, the method of choice is to—one way or another—make the working class pay. We need look no further than Canada’s own history for an example.

Struggling to deal with the fallout from the economic crisis of the 1970s, successive Liberal and Conservative governments carried on a borrowing binge that brought debt as a proportion of GDP from 23 per cent in 1969 to 100 per cent by 1995.

Lenders panicked. In 1992, Standard & Poor’s downgraded Canada’s credit rating. Moody’s followed suit in 1994. In 1995, international finance capital became so alarmed that they began to apply serious pressure. The Wall Street Journal ran an editorial calling Canada “an honorary member of the Third World” and dubbed the Canadian dollar the “northern peso.”

By 1994, a tipping point was reached. Investor confidence plummeted, and borrowing rates surged from an already high seven per cent to an imminently dangerous nine per cent in a matter of months. A spiral of rising interest rates and plummeting lender confidence had begun.

The government was able to restore investor confidence and save the situation by balancing the budget—at the expense of the working class. Prime Minister Jean Chrétien and his hatchet man, Finance Minister Paul Martin—ever ready to please their corporate paymasters—swiftly imposed a 10 per cent reduction in social spending. These were the deepest cuts in Canadian history. Their effects can still be felt, through crumbling infrastructure, schools and hospitals.

All roads lead to austerity

Today, the situation the government faces is even worse. Canada’s economy is in a far worse state, there is less fat to cut from the budget, and the government’s military spending is set to consume $160 billion annually by 2035.

The warning lights are already flashing. For more than 20 years, Canada has held an AAA credit rating, the highest possible, indicating that creditors consider the risk of default to be virtually nil.

Several provinces have already had their ratings downgraded—including Alberta, which has been downgraded six times! The federal government’s rating is also at risk. Randall Bartlett, an economist at Desjardins Group, recently warned that “Canada’s AAA status shouldn’t be taken for granted,” suggesting that while an immediate downgrade is unlikely, if the government can’t get the problem under control, it could threaten the country’s sterling credit reputation. Meanwhile, the effects of Trump’s tariffs and rising geopolitical instability are feeding back into the economy, pushing inflation upward, which risks raising interest rates even higher.

These are early signs that Canada’s debt is unsustainable. A reckoning is inevitable at one point or another, unless the deficit is brought down.

Crisis of Canadian capitalism

The only way to avoid austerity is growth. That’s why the new spending in the 2025–26 budget is being touted as a means of “supercharging” the economy by creating the conditions for a mind-boggling one trillion dollars in investment in the next five years. The government claims this will create hundreds of thousands of middle-class jobs, raise the average wage by more than $3,000 per year, and catapult Canada into position as the strongest economy in the G7. If this happens, revenues will rise alongside living standards, and paying down the debt will no longer be a problem.

This begs the question: if it were that easy to turn Canada into the “strongest economy in the G7”, why hasn’t it been done already? Also, if Carney’s policy could transform the economy, it follows that it would have to be somehow different from what came before it. In reality, Carney’s deficit financing magic is the same old song and dance that every successive government has performed since 2008. It is exactly what got the government into this mess in the first place, as debt was used to prop up the ailing economy and failed to stimulate genuine investment in production.

The only serious difference between Carney’s policy and that of those who came before is the massive increase in military spending. But as we have explained elsewhere, the majority of this will end up in the pockets of foreign companies. While it can temporarily employ workers in arms production, it sucks much needed investment out of the real economy, acting as an immense drain. Arms expenditure is therefore inherently inflationary because it increases demand without increasing productivity.

Worse still, the debt crisis is not specific to the government, but is in fact generalized in Canadian society. Households carry a debt load equal to 108 per cent of GDP, while corporate Canada’s debt totals 163 per cent of GDP. Debt thus strikes from both sides: on the one hand, consumer debt discourages consumption, as a bigger and bigger proportion of the income of the working class goes toward paying down mortgage and credit card debts; while on the other hand, massive corporate debts put downward pressure on new investment. These debts hang like an albatross around the neck of the Canadian economy and make it even less likely that a revival is possible.

The root of the problem is that the debt is not an isolated issue, but just one manifestation of the deep crisis of Canadian capitalism itself. Since 2008, the economy has been stagnant; now the realignment of world relations and U.S. imperialism’s abandonment of the post-war order are turning a crisis into a complete catastrophe.

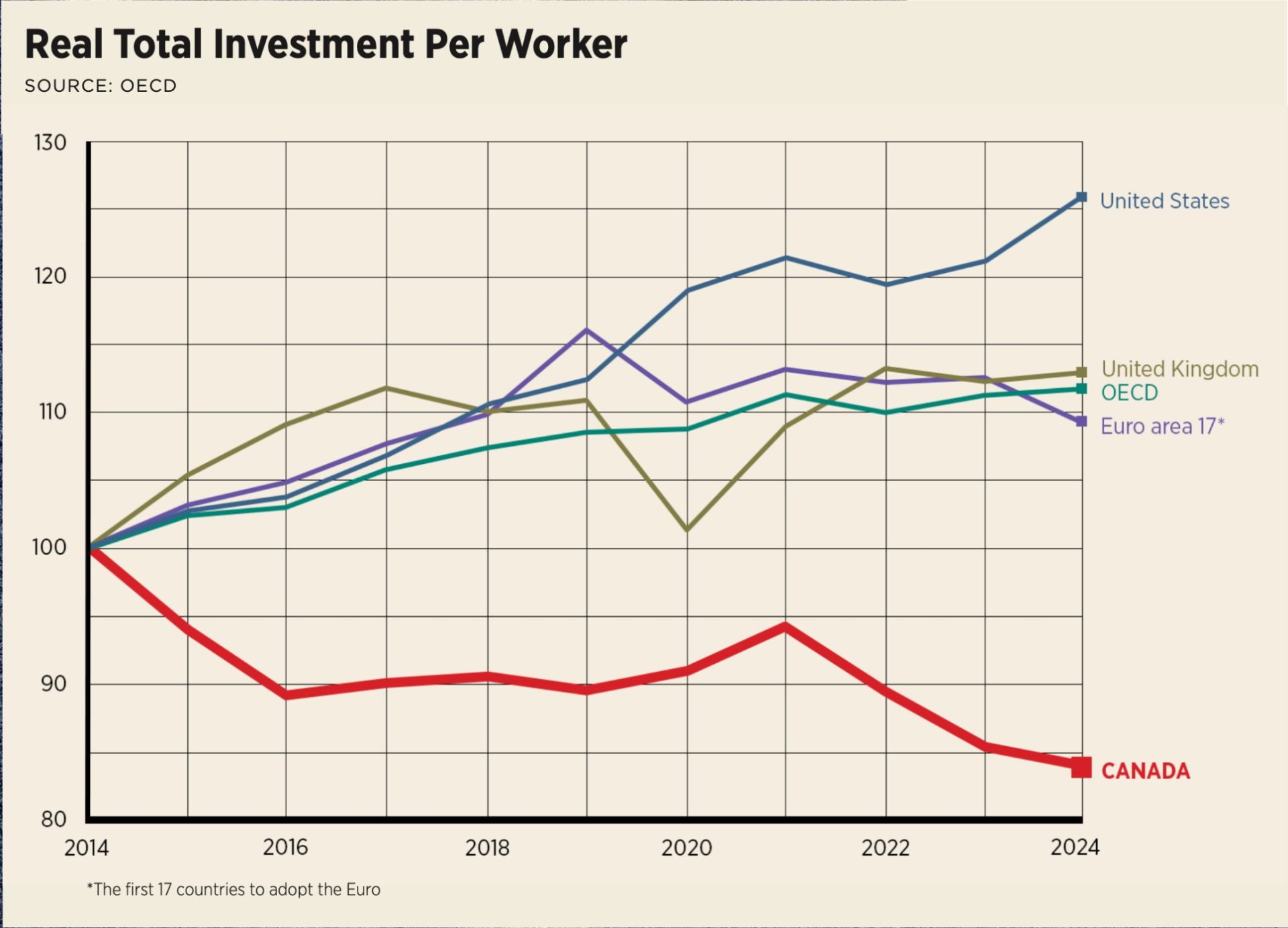

Both domestic and foreign capital are fleeing the country. This has created what one think-tank called an “investment crisis”. Investment per worker has been on the decline since 2024. And as of 2024, Canadian investments abroad totaled $2.3 trillion, while foreign investment in Canada totaled only $1.3 trillion—a one trillion dollar difference.

This collapse in capital investment is reflected in Canada’s labour productivity, the measure of economic output per hour worked. Investment in machinery—which increases productivity—has plummeted to its lowest level since records began in 1981. Canadian productivity has been declining relative to the U.S. since the 1980s, and in the last few years it has started to decline in absolute terms, falling by 1.2 per cent since 2022. According to the most recent estimates, Canada is only able to muster about 70 per cent of U.S. labour productivity.

This means that Canadian workers are paid higher wages to produce less than in other countries, making Canadian exports uncompetitive and discouraging investment further. After all, from the point of view of a capitalist, why pay a low-productivity worker a high wage in Canada when you could extract the same value from a low-wage worker elsewhere?

In order to make Canadian goods competitive on the world market, productivity must be brought in line with wages and working conditions. This means one of two things: either a massive investment in industry and machinery to raise productivity—which the capitalists will only do if they are guaranteed a profit—or massive cuts to the living standards of Canadian workers.

The reaction of the corporate elite to Carney’s budget shows the path they intend to take. The Globe and Mail called it a “milquetoast effort”, while the Business Council of Canada complained that it “doesn’t go far enough and fast enough to attract investment and strengthen competitiveness.” The meaning of this is clear: massive pressure is being placed on the government to slash budgets and cut regulations so that Canada’s bosses can drive wages and working conditions to the very bottom.

Overproduction

None of this would be reason for concern if the world market were desperate for industrial goods. If there were an excess of demand over supply, Canadian goods would still find a market, investment would flow in, and productivity would rise as a matter of course. But the reality is the opposite—capitalism is bogged down in a deep crisis of overproduction all over the world.

Overproduction is the fundamental cause of crisis under capitalism. As capitalists compete with each other for market share, they are constantly compelled to invest to produce more commodities, faster and more cheaply. On the other hand, the working class, which is the bulk of the consumer market, is not paid the full value of what it produces, and thus cannot afford to buy all the products it creates.

This is exactly the state of affairs in Canada today, where the ruling class now prefers to parasitically invest in unproductive speculation, especially in real estate. Hence the rise of the housing bubble. And on top of this existing crisis is the trade war with the U.S., the most important consumer market and recipient of around 70 per cent of Canada’s exports.

All the means at Carney’s disposal—from direct corporate subsidies, to tax incentives, to building infrastructure, to military contracts—have to contend with the reality that the world market is limited and Canada is uncompetitive on it.

That is why private industry is not investing, despite Carney’s measures. For example, the government hopes to develop the rare earth minerals industry. But even after providing billions in handouts and so-called “offtake agreements” which pass off all the risk from the capitalist onto the taxpayer, these new mining projects are failing to secure private investment because investors are worried that they cannot compete with cheaper minerals from China, which dominates that market.

Another example is Canada-based Nutrien, the world’s largest producer of potash, which—in a fine display of “elbows-up” patriotism—abandoned plans to construct a new export terminal in British Columbia in favour of a more profitable location in Washington.

As for the auto industry, despite hundreds of millions in subsidies, Stellantis and GM have both recently moved production from Ontario plants to the U.S., citing the difficulty of making a profit by producing in Canada.

These are just a few examples that demonstrate the harsh reality. Whatever the government does, unless the fundamental uncompetitiveness of Canada is solved through tax cuts, cuts to regulations, and unprecedented attacks on wages and working conditions, the government’s efforts to attract investment are like bailing water out of the Titanic with a bucket.

While Carney may succeed in attracting some industrial investment, this will not overcome the economic crisis or reverse the investment crisis. Capitalists will simply pocket the government’s money, as they did during the pandemic, then continue investing where it’s most profitable—that is, not in Canada.

Class struggle is inevitable

Marx and Engels wrote almost 200 years ago in the Communist Manifesto: “And how does the bourgeoisie get over these crises? […] by paving the way for more extensive and more destructive crises, and by diminishing the means whereby crises are prevented.”

This is precisely the situation today. Ever since 2008, the ruling class has taken on mountains of debt to prop up the economy while trying to maintain living standards, and in this way stave off the pitchfork rebellion that austerity would produce. The debt is symptomatic of the deep crisis of Canadian and world capitalism.

And now the ruling class is out of options and is left with no alternative—except to make the working class pay. Instead of delaying the crisis, the debt has become an explosive factor in an already explosive crisis.

Canada’s corporate elite has finally lost patience, and is baying for blood. Their attitude was captured in a recent Globe and Mail article lamenting the cost of a new benefit meant to ease rising grocery costs for working class families:

“This year’s deficit was already predicted to be an eye-watering $78.3-billion. Without offsetting changes, the program announced Monday would push that number well past $80-billion. Sooner or later (sooner we hope), Mr. Carney will need to ask Canadians to sacrifice, and stop pretending that the billions of dollars the Liberals periodically dole out come without cost or consequence.”

This is the authentic voice of the Canadian ruling class. To save their system, all means are justified—so long as they don’t have to pick up the cheque. The “sacrifice” will fall on the backs of those least able to bear it.

The magnitude of austerity needed to restore economic equilibrium will be colossal. Living standards will tank. Health care, education and pensions will be obliterated. Mass public sector layoffs and privatizations will be the new normal. Canada will become completely unrecognizable.

But this is only one side of the coin. The demon the ruling class tried to exorcise through deficit financing—the class struggle—will come back with a vengeance. If Canadian workers want a glimpse of their own future, they should look to France, where the attempt to solve the debt crisis with austerity gave birth to the “Bloquons tout” movement, a mass uprising that has shaken the country and reverberated throughout Europe. It is only a matter of time before titanic class battles just like these come to Canada.